Effective Date: April 1, 2026

Preface

For years, Indian businesses treated digital bookkeeping as a matter of convenience rather than a strict legal mandate. Effective April 1, 2026, with the enforcement of Rule 46(8) under the Income-tax Rules 2026, the Central Board of Direct Taxes (CBDT) has shifted the goalposts, from simple data storage to “verifiable digital integrity”, if data is maintained in electronic format.

If your business maintains electronic records, simply having the data is not enough. You must now prove its authenticity through a strict, India-based framework. This article examines the text of the Rule, interprets its key provisions, traces its legal lineage, and offers practical guidance for compliance.

Rule 46(8) of the Income-tax Rules 2026

Section I: Scope and Applicability

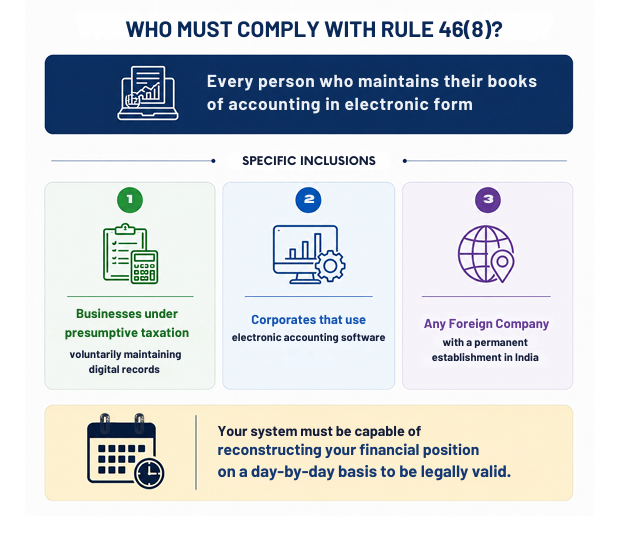

Who Is Covered?

The concept of verifiable digital integrity under Rule 46(8) applies to every person who maintains their books of accounting in electronic form, whether a sole proprietor, partnership firm, limited liability partnership, private or public company, or any other taxable entity under the Income-tax Act, 2025. The Rule is not sector-specific; it applies uniformly across industries.

Entities specifically within scope include:

- Businesses filing under the presumptive taxation scheme (Sections 58) that nonetheless maintain digital records voluntarily

- Corporates that use electronic accounting software

- Foreign companies with a Permanent Establishment (PE) in India, to the extent their books covering Indian operations are maintained digitally

What Constitutes “Books of Account” Under the Rule?

The expression “books of account” under Section 2(19) of the Income-tax Act, 2025 includes ledgers, day books, cash books, account books, and other books, whether maintained manually or in digital form or printouts of data maintained in digital form. Under Rule 46(8), the digital equivalent must meet the same structural standards as physical books: it must support reconstruction of the financial position on a day-by-day basis.

Interpretation: A mere transaction log, CSV export, or raw database table does not constitute “books of account” in the statutory sense unless it is structured to reflect complete ledger entries, supports detailed view from summary to voucher level, and captures the audit trail of modifications.

Section II: The Core Mandates of Rule 46(8)

Rule 46(8) introduces two mandatory requirements:

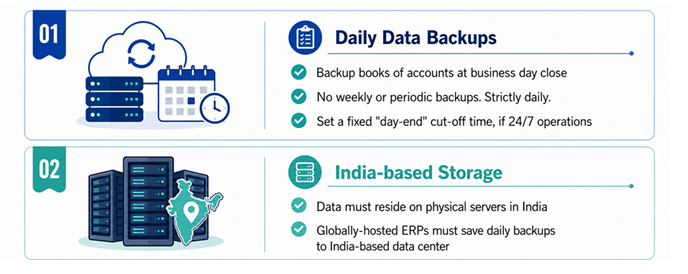

Mandate 1: Daily Backups

Every entity maintaining electronic books must take a backup of books of account on a daily basis at the close of each business day. This is not a weekly or periodic requirement; it is strictly daily.

Interpretation of “Daily”: The Rule’s use of “daily” must be read strictly. A backup taken at the end of a business day satisfies the requirement for that day. However, entities that operate across time zones or run 24-hour operations must establish a fixed “day-end” cut-off time, document it as policy, and maintain backups at that fixed interval consistently. Random or irregular backups, even if taken frequently, would not satisfy the literal intent of the provision.

Mandate 2: Data Localization — Storage on Indian Servers

The backup must be stored on servers physically located within India daily. This applies even if the primary accounting system or ERP is hosted on a global cloud infrastructure (eg, AWS, Azure, or Google Cloud data centres outside India).

Interpretation of “Servers Located in India”: This provision has significant implications for multi-national cloud deployments. A business using a globally distributed cloud must ensure that backup replication is configured to an India-region node specifically. Mere contractual assurances from a foreign vendor that “data may be processed in India” are insufficient. The obligation is jurisdictional and physical. So, the storage medium must be within Indian territory.

Section III: Why a “Database Dump” Is Not Compliant

Many IT teams believe that a weekly SQL dump or a CSV export of transactions satisfies the “electronic records” requirement. Under Rule 46(8), this is a risky misconception.

3.1 Absence of Audit Trail and Chronology

A database dump is typically a snapshot of the current state of data. It captures what the records look like at a point in time, not how they evolved. Rule 46(8), read alongside the Companies (Accounts) Rules, 2014 (as amended), which is applicable to Companies, requires that accounting software record an audit trail of every transaction, including the date and time of each creation, alteration, or deletion maintaining the history of values.

A raw dump is “dead data.” It lacks the living history that a tax officer needs to verify that entries were not manipulated after the close of accounts.

Interpretation: The audit trail requirement is not satisfied by version-control systems like Git either, unless those systems are integrated with the accounting software itself and capable of recording user-level transaction histories. The trail must be embedded in the accounting record, not maintained as a parallel IT record.

3.2 The “Regularly Kept” Standard Under Section 34

Section 34 of the Indian Evidence Act, 1872 (now the Bharatiya Sakshya Adhiniyam, 2023) provides for the admissibility of entries in books of account, but only if those books are regularly kept in the course of business. In the landmark case of Central Bureau of Investigation v. V.C. Shukla (1998), the Supreme Court clarified that entries must be part of books maintained in the ordinary course of business to qualify as evidence.

Interpretation: A database dump generated specifically for a tax audit, rather than maintained continuously, would likely fail this test. The regularity of maintenance in its original form as created at the time of transactions, not the completeness of the data, is what gives legal validity. Rule 46(8)’s daily backup mandate is essentially a formalisation of this “regularity” standard for the digital age.

3.3 Acceptance as Evidence Under Section 65B

To use electronic records as evidence before an Assessing Officer (AO) or the Income Tax Appellate Tribunal (ITAT), a taxpayer must satisfy Section 65B of the Indian Evidence Act (Section 63 of the Bharatiya Sakshya Adhiniyam, 2023). This section requires:

That the computer was in regular use at the time the record was produced;

That the computer was operating properly;

That the information was fed into the computer in the ordinary course of activities; and

That a certificate to this effect is produced, signed by a responsible official.

Section IV: Intersection With Other Laws

Rule 46(8) does not operate in isolation. It must be read alongside several related laws:

4.1 The Companies Act, 2013 — Section 128 and MCA Notification

Section 128(1) of the Companies Act requires every company to maintain its books of account at its registered office. The MCA Notification dated 31st March 2022 further clarified that companies using accounting software must ensure the software has an audit trail feature that cannot be disabled. Rule 46(8) reinforces this for income-tax purposes, creating a dual compliance obligation for corporate taxpayers.

4.2 The Information Technology Act, 2000 — Section 7A

Section 7A of the IT Act recognises the legal validity of electronic records and the obligation to maintain the same for audit purpose.

Businesses maintaining digital books under Rule 46(8) should also ensure that their backup and storage systems conform to provisions related to data integrity and access controls.

Section V: Penalties for Non-Compliance

Section 441 — Failure to Keep and Maintain Books

Section 441 of the Income-tax Act empowers the Assessing Officer to levy a penalty of up to ₹25,000 for failure to keep and maintain books of account as required under Section 62. Non-compliance with Rule 46(8), which prescribes the manner of maintaining digital books, falls within this provision.

Interpretation: The penalty under Section 441, while modest in absolute terms, is not the primary risk. The greater exposure is that an AO who finds non-compliance with Rule 46(8) may treat the taxpayer’s books as not duly maintained. This opens the door to best-judgment assessment under Section 271, where the AO may estimate income on the basis of available material, often adversarial. This is a far more consequential outcome than the ₹25,000 penalty.

Section VI: The Compliance Workflow

To stay on the right side of the law, businesses must transition from manual backups to automated, localised systems. A compliant workflow should include:

- Automated End-of-Day Backup Trigger: Configure your ERP or accounting system to automatically initiate a backup at a defined cut-off time each business day.

- India-Region Storage Destination: Map the backup destination explicitly to an India-region cloud node (eg, AWS ap-south-1, Azure India Central) or an on-premise server within India.

- Backup Log Maintenance: Maintain a timestamped log of each backup event, including the date, time, size of the backup, and a cryptographic hash (MD5 or SHA-256) of the backup file. This log is your primary evidence of daily compliance.

- Audit Trail Verification: Periodically verify that your accounting software’s audit trail is intact and has not been disabled, particularly after software updates or system migrations.

- Section 65B Certificate Readiness: Designate a responsible officer who can sign the Section 65B certificate in the event of an assessment and ensure that your IT team can produce a certificate attesting to the system’s regular use and proper functioning, if need be.

Section VII: Practical Steps for Businesses

- Audit Your Cloud Vendor: Ensure your ERP or accounting provider offers India-specific data residency. Request a written confirmation specifying the physical location of the storage node.

- Integrate Payroll Systems: Since payroll is a significant expense item reflected in books of account, your HR and payroll system must be integrated with your accounting system and equally subject to data localisation norms. Ensure your HRMS provider offers compliant India-hosted data storage.

- Review Third-Party Integrations: Payment gateways, invoicing platforms, Payroll software, GST filing tools that provides for data exchanges from/to your accounting software, must also be audited for their backup and residency practices and ensure audit trail covers the same.

- Verify the Backup Log Regularly: Do not wait for a notice from the AO. Conduct quarterly internal audits to confirm that daily backups are being taken and that the log is intact and producible.

- Train Responsible Personnel: Designate a compliance officer familiar with both the IT infrastructure and the income-tax requirements to own this obligation.

Conclusion

Rule 46(8) goes beyond a technicality of record-keeping, it is a transparency and governance initiative. It reflects the broader legislative push toward verifiable, tamper-proof financial records in the digital economy. By mandating daily backups in India with a permanent audit trail (applicable for Companies), the CBDT has set clear legal standards for electronic records. This aligns with what courts have long expected.

The ₹25,000 penalty under Section 441 is one risk for non-compliant businesses. They may also face best-judgment assessments and the fulfillment of requirement for certification of electronic records under Section 65B.

Businesses that treat Rule 46(8) as a box-ticking exercise miss the larger point. In the event of a dispute, the integrity of your digital books is your single most important line of defence.

The time to build that defence is not when a notice arrives. It is now.

Author Bio

K B Muralidharan, B.Com. FCA, Grad. C.W.A, D.I.S.A. (ICA)

K B Muralidharan, B.Com. FCA, Grad. C.W.A, D.I.S.A. (ICA)

Practicing Chartered Accountant and is in practice since 1996. Participated as a member of Study Group constituted under the auspices of Southern India Regional Council of ICAI for preparation of Background Material for Continuing Education Programs on Audit of General Insurance Companies. Also served as a visiting faculty in Commerce Department, A.M. Jain College, Chennai for three years.

*This article is intended for informational purposes only and does not constitute legal or tax advice. Businesses should consult their tax advisors for guidance specific to their circumstances.