What the Replacement of IAS 1 Means for Your Organisation

— and How Sage Intacct Can Make the Transition Seamless

| What Is IFRS 18?

IFRS 18 (International Financial Reporting Standard 18) is a new accounting standard introduced by the International Accounting Standards Board (IASB) that replaces IAS 1. It introduces mandatory income statement categories, a standardised operating profit subtotal, and new disclosure rules for management-defined performance measures (MPMs). Effective from 1 January 2027 with retrospective application, it is the most significant overhaul of financial statement presentation under IFRS in a generation. |

Why Did the IASB Replace IAS 1 with IFRS 18?

The old financial presentation rules no longer fit the modern business era. With IFRS 18, the IASB aims to close the transparency gaps and implement a reporting upgrade for better investor confidence.

Here are the core reasons behind the biggest accounting shift in decades:

1. Lack of Uniformity in Income Statement Structures

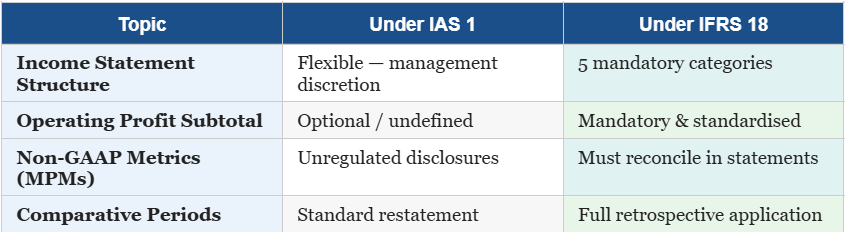

IAS 1 lacks a clearly defined structure for the Income Statement. As of now, companies are free to choose their own subtotals to include, which leads to various confusions while comparing the core profitability of companies operating in the same industry. IFRS 18 introduces operating, investing, and financing categories, enabling clearer benchmarking and facilitating direct comparison for comparing a company’s performance.

2. Lack of Transparency in Company-specific Performance Metrics

As of now, many companies share non-standard financial metrics without detailing how to calculate them. This lack of transparency undermined investor confidence, as they cannot independently verify the numbers’ authenticity. IFRS 18 aims to improve visibility for the investors and enhance their confidence. It mandates explanations of these company-specific measures so that investors can independently audit the management-defined performance measures.

3. Inadequate Breakdown of Material Expenses and Vague Grouping

Many companies followed a practice of aggregating massive amounts of diverse expenses into vast, vaguely labeled categories. Modern accounting standards demand extreme comparability, structure, and auditability. With IFRS 18, the focus is on disciplined structure and avoiding critical operational realities (such as sudden spikes in specific overhead costs) that were hidden from view.

The Three Structural Pillars of IFRS 18

1. Mandatory Income Statement Categories

Under IFRS 18, every item of income and expense must be classified into one of five defined categories: Operating, Investing, Financing, Income Taxes, and Discontinued Operations. This replaces the latitude previously afforded to management, who could largely determine how line items were labelled and grouped.

For many organisations — particularly those in financial services, real estate, or complex holding structures — reclassifying existing Chart of Accounts items into these categories will require a methodical, transaction-by-transaction review. Finance systems that lack dimensional flexibility will face significant reconfiguration costs.

- Operating: core business activities

- Investing: returns on investments not classified as associates/subsidiaries

- Financing: costs of financing the entity’s activities

- Income Taxes: current and deferred tax

- Discontinued Operations: separate from continuing activities

2. Mandatory Operating Profit Subtotal

Perhaps the most immediately visible change for preparers is the introduction of a standardised, mandatory operating profit subtotal. Under IAS 1, entities could present operating profit — or omit it entirely — at their discretion, resulting in wildly different definitions across sectors and jurisdictions.

IFRS 18 ends that ambiguity. Operating profit becomes a defined, non-negotiable line item in every IFRS-compliant income statement. Finance systems must be reconfigured to compute and present this figure in conformity with the IASB’s definition, not management’s preference.

3. Management-Defined Performance Measures (MPMs)

The most far-reaching provision targets Management-Defined Performance Measures (MPMs) — headline figures such as “Adjusted EBITDA” or “Underlying Operating Profit” communicated in earnings releases and investor presentations.

Under IFRS 18, if an entity publicly communicates an MPM, it must be reconciled back to the closest IFRS-defined subtotal within the formal financial statements themselves, complete with the tax effect of each adjustment. This is a seismic shift: MPMs that previously lived exclusively in investor packs — unaudited and unchallenged — must now be disclosed and reconciled within audited accounts.

Why the Transition Challenge Is Greater Than It Appears?

IFRS 18 requires full retrospective application — meaning entities must restate comparative periods. For a December year-end, that means 2026 comparatives must be restated under the new framework. Organisations that begin their transition assessment in late 2026 will face an unmanageable sprint.

The compliance challenge is not cosmetic. It requires finance teams to: revisit the Chart of Accounts architecture, redesign financial reporting templates, establish new MPM disclosure workflows, restate comparatives, and train stakeholders on restated figures. For organisations relying on legacy ERP platforms with rigid reporting structures, the 2027 deadline is already approaching.

How Sage Intacct Positions Organisations for IFRS 18 Success?

Sage Intacct — the cloud-native financial management platform purpose-built for the modern finance function — provides the structural flexibility and reporting intelligence needed to navigate the IFRS 18 transition with confidence. Its architecture directly addresses each of the three pillars.

1. Flexible Dimensional Chart of Accounts

Sage Intacct’s multi-dimensional account structure enables finance teams to tag every transaction across multiple dimensions — entity, department, project, location, and custom classifications. Reclassifying income and expenses into IFRS 18’s five mandatory categories becomes a configuration exercise, not a data overhaul. New dimensions can map existing transactions to the new categories without compromising historical data integrity.

2. Configurable Financial Reporting

Sage Intacct’s reporting engine allows finance teams to build the precise income statement structure that IFRS 18 mandates — including the required operating profit subtotal — without IT intervention. Report templates can be updated, version-controlled, and deployed across group entities, ensuring consistency for consolidation and group reporting purposes.

3. MPM Disclosure Automation

Reconciling MPMs under IFRS 18 requires tracing every adjustment from a publicly communicated metric back to IFRS line items — with tax effects. Sage Intacct’s real-time reporting and drill-down capability make this audit trail transparent and auditor-ready, dramatically reducing the manual effort traditionally associated with disclosure preparation.

4. Audit-Ready Comparative Period Restatement

IFRS 18’s retrospective application demands restated comparatives. Sage Intacct’s historical data retention and period-comparison reporting means organisations can generate restated 2026 figures alongside 2027 actuals — without rebuilding reports from scratch, and without relying on error-prone spreadsheet bridges.

5. Built for Your Industry’s Unique Requirements

Sage Intacct is built to mitigate the unique challenges faced by each industry. With deep industry knowledge built into the system, it takes your business a step further by providing unique workflows, advanced functionality, reporting, and customization requirements tailored for your industry. It offers customized solutions for financial services, wholesale distribution, healthcare, Software as a Service (SaaS), hospitality, professional services, and many other industries operating in India.

The Bottom Line

IFRS 18 is not an incremental update — it is a foundational rethink of how financial performance is communicated under IFRS. The 2027 effective date may appear comfortable, but the need to restate 2026 comparatives means that preparation must begin in 2025. Organisations that invest now in systems-readiness — leveraging platforms like Sage Intacct — will not only achieve compliance but will emerge with more transparent, comparable, and decision-useful financial reporting.

The standard is clear. The timeline is fixed. The question is: Is your finance system ready?

Frequently Asked Questions

| 1. When does IFRS 18 become effective?

IFRS 18 is mandatory for annual reporting periods beginning on or after 1 January 2027, with full retrospective application. Early adoption is permitted. Most calendar-year-end entities will need restated 2026 comparatives ready by early 2028. |

| 2. Does IFRS 18 replace IFRS 15 (Revenue)?

No. IFRS 18 replaces IAS 1, which governs the presentation and disclosure of financial statements. IFRS 15, the revenue recognition standard, remains fully in force and is unaffected by IFRS 18. |

| 3. What are Management-Defined Performance Measures (MPMs) under IFRS 18?

MPMs are subtotals of income and expense communicated outside the financial statements (e.g. in earnings releases) that are not defined or specified in IFRS. Under IFRS 18, entities must disclose and reconcile all publicly communicated MPMs within the formal financial statements, including the related tax effects. |

| 4. How does Sage Intacct help with IFRS 18 compliance?

Sage Intacct’s multi-dimensional Chart of Accounts, configurable reporting engine, real-time drill-down capability, and historical data retention directly address IFRS 18’s three pillars: mandatory income statement categories, the standardised operating profit subtotal, and MPM reconciliation disclosures. To better understand how Sage Intacct maps to your specific operational workflows, explore the Sage Intacct Product Brochure that provides valuable technical and functional insights into the product. |

| 5. What is the best way to transition an existing financial system to meet IFRS 18 standards?

Aligning your existing financial reporting with the IFRS 18 standards would require process evaluation and software configuration. To move legacy data securely and maintain consistency across all platforms, it’s highly recommended to collaborate with Sage Intacct migration services offering comprehensive support and certified professionals. |

Author Bio

Jitendra Somani is a senior finance and accounting professional with dual professional designations: Associate Chartered Management Accountant (ACMA) and Chartered Global Management Accountant (CGMA®) from the Chartered Institute of Management Accountants (CIMA), UK, and a member of the Institute of Public Accountants (IPA), Australia. With deep expertise spanning IFRS adoption, financial transformation, and cloud ERP implementation — including Sage Intacct — Jitendra advises organisations navigating complex accounting standard transitions. Connect on LinkedIn.

Jitendra Somani is a senior finance and accounting professional with dual professional designations: Associate Chartered Management Accountant (ACMA) and Chartered Global Management Accountant (CGMA®) from the Chartered Institute of Management Accountants (CIMA), UK, and a member of the Institute of Public Accountants (IPA), Australia. With deep expertise spanning IFRS adoption, financial transformation, and cloud ERP implementation — including Sage Intacct — Jitendra advises organisations navigating complex accounting standard transitions. Connect on LinkedIn.

Credentials: ACMA • CGMA® (CIMA, UK) • IPA Member (Australia)

© 2026 Jitendra Somani. The views expressed are the author’s own and do not constitute formal accounting or legal advice.