What is of Factory Overhead?

Factory Overhead includes all those expenses incurred for the manufacturing of the company’s products that cannot be directly attributed to any single specific product such as factory rent, machine maintenance, machine upgradation, depreciation on fixed assets, and administrative costs, among others.

Factory Overhead impacts the company’s Income Statement as well as Balance Sheet. It is shown under the Cost of Goods Sold (COGS) section of the Income Statement, and the Current Assets section of the Balance Sheet.

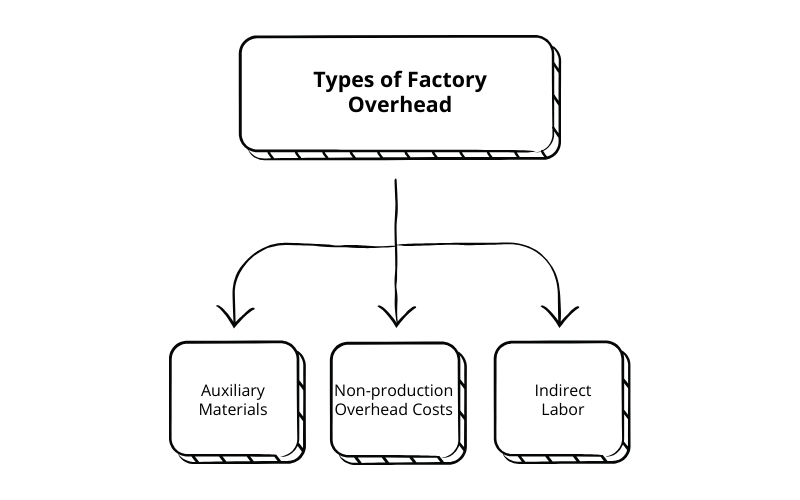

What are the Different Types of Factory Overhead?

Here are the three types of Manufacturing Overhead:

1. Auxiliary Materials

Auxiliary materials include materials that are used for continuing the production activity, however, they are not part of the final product manufactured by the company. These materials are extremely crucial to sustain the company’s production activity. Examples include personal protective equipment, disposable gloves, cleaning materials, tapes, etc.

2. Non-production Overhead Costs

Non-production Overhead Costs are considered variable expenditures because of their fluctuating nature. These include licensing costs, utility bills, fire insurance premiums, depreciation on fixed assets, factory maintenance costs, etc.

3. Indirect Labor

Indirect laborers are not involved in the conversion of raw materials into finished goods. Thus, any salaries paid to these laborers are not directly aligned with the company’s production activity. Examples of indirect labor include clerks, Quality Assurance Officers, Accounting Managers, Financial & Cost Accountants, etc.

What is Factory Overhead Formula?

Manufacturing Overhead relates to the manufacturing industry. There are different ways to calculate it.

1. Factory Overhead

The Manufacturing Overhead formula is concise, simple, and straightforward. A common thing between all of the expenditures included in it is that they are all incurred for the production of goods. However, none of these expenditures are directly related to any specific product manufactured.

Factory Overhead = Indirect Labor + Indirect Materials + Other Manufacturing Overhead Costs

2. Fixed Manufacturing Overhead (FMOH)

Fixed Manufacturing Overhead contains those overhead costs that are not dependent on the production volume such as the rent of the production factory, salaries paid to the direct labor, and depreciation of capital assets (such as furniture, building, office equipment, etc.)

Formula:

Fixed Manufacturing Overhead = (Total Fixed Costs − Variable Costs per Unit) * Number of Units Produced

3. Variable Manufacturing Overhead (VMOH)

Variable Manufacturing Overhead is the sum of all the factory overhead costs. VMOH may differ by the change in the production volume. Examples of VMOH include electricity charges, water & fuel charges, etc.

Formula:

Variable Manufacturing Overhead = Variable Overhead Rate * Number of Units Produced

4. Semi-variable Manufacturing Overheads (SVMOH)

Semi-variable Manufacturing Overheads are nothing but a mix of both the fixed & variable types of manufacturing overheads. These are the expenditures that a business must incur whether the production activity is ongoing or stopped. Examples include utility bills and commissions paid.

Formula:

Semi-variable Manufacturing Overheads = Fixed Cost + (Per Unit Variable Cost * Total Units)

5. Applied Manufacturing Overhead (AMOH)

Applied Manufacturing Overhead is a method used to calculate the overhead costs that are unique to a specific product. It provides various benefits from reducing costs, supporting better decision-making, and evaluating performance. It is an effective measure for cost control, and identifying the impact of production levels on the company’s profitability.

Formula:

Applied Manufacturing Overhead = Predetermined Overhead Rate * Actual Activity

6. Percentage of Direct Material Cost

Percentage of Direct Material Cost is one of the most commonly used formulas. Use the following formula if the Factory Overhead cost is a substantial amount of the Total Cost. Calculating the Percentage of Direct Material Cost allows your business to take various cost control measures and set better pricing strategies.

Formula:

Overhead Rate = (Direct Material Cost / Factory Overheads) * 100

7. Percentage to Direct Labor Cost

Percentage to Direct Labor Cost indicates the percentage of total factory overhead attributed to direct labor expenditures. Much like other ratios, it is also indicated in percentage. You may use this formula to evaluate the effectiveness of your production workforce in relation to the overhead expenditures and take measures to improve efficiency.

Formula:

Percentage to Direct Labor Cost = (Direct Labor Cost / Total Factory Overhead) * 100

8. Percentage to Prime Cost

The Percentage to Prime Cost method indicates the percentage ratio of factory overhead costs to the prime costs. The purpose of using this method is to gain a better understanding of the contribution of Factory Overhead towards the Prime Cost. Percentage to Prime Cost formula will help you with accurate financial planning and analysis.

Formula:

Percentage to Prime Cost = Factory Overhead Costs / Prime Cost ) * 100

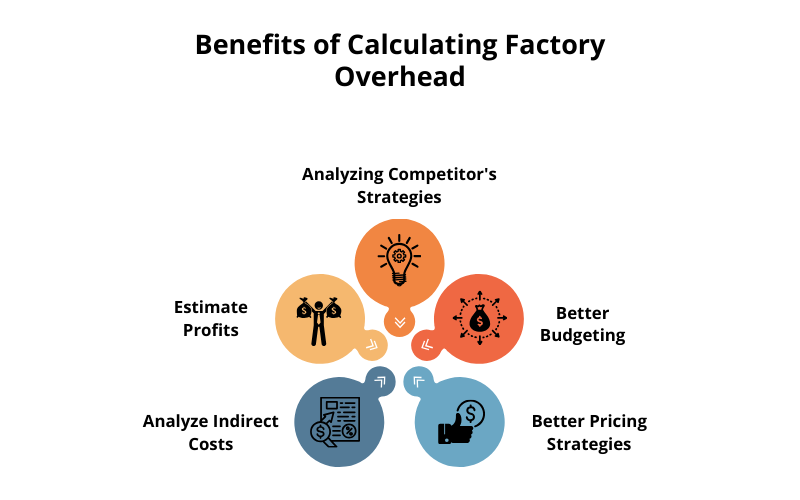

What are the Benefits of Calculating Factory Overhead?

Now, let’s discuss how calculating the Factory Overhead will provide you with a competitive advantage and face modern business challenges.

1. Evaluate Financial Position

Profit maximization is the ultimate objective of any business regardless of its size and type. Factory Overhead accounts for all the company’s indirect expenditures and investments. Calculating it is important to evaluate the financial position of the company, identify new growth opportunities, and find areas of improvement.

2. Set Better Pricing

Factory Overhead allows you to set better pricing strategies by gaining a better understanding of the indirect costs that need to be covered to maximize the profit margin. Setting optimum pricing will help your business sustain itself in the long run.

3. Track Expenses Diligently

A company must track its indirect costs and find ways to reduce them to improve profitability. Manufacturing ERP software plays an important role in cost-cutting, tracking expenses diligently, and optimizing your pricing strategies.

4. Better Respond to Changes

Factory Overhead aids budgeting by helping you set clear and realistic goals to achieve the strategic objectives of your company. Eventually, your company will cut down expenditures, efficiently use its resources, and better respond to market changes with strategic decisions.

5. Competitor Analysis

Another benefit of calculating Factory Overhead with an ERP application is that it allows you to analyze the strengths and weaknesses of your competitors, and determine their resource efficiency & level of operational efficiency. You can fine-tune your existing strategies to gain a competitive advantage.

What are the Limitations of Manufacturing Overhead?

While Operational Overhead is an important concept to evaluate the costs, bring down manufacturing cost, and improve profitability, it has certain limitations too.

1. Inaccurate Projections

There are times when the Manufacturing Overhead cost estimations may go wrong and yield incorrect estimations, leading to strategically incorrect decisions.

2. Labor-intensive Task

Calculating Manufacturing Overhead can be a time and labor-intensive task. However, the best ERP software in India should automate & simplify mundane tasks and help operate your business smoothly.

3. Limited Scope

Production Overhead is used to evaluate only indirect costs. Some of these costs can be difficult to control.

4. Omits Direct Labor Costs

Direct labor and direct material costs are significantly higher for many businesses. Manufacturing Overhead does not include these costs.

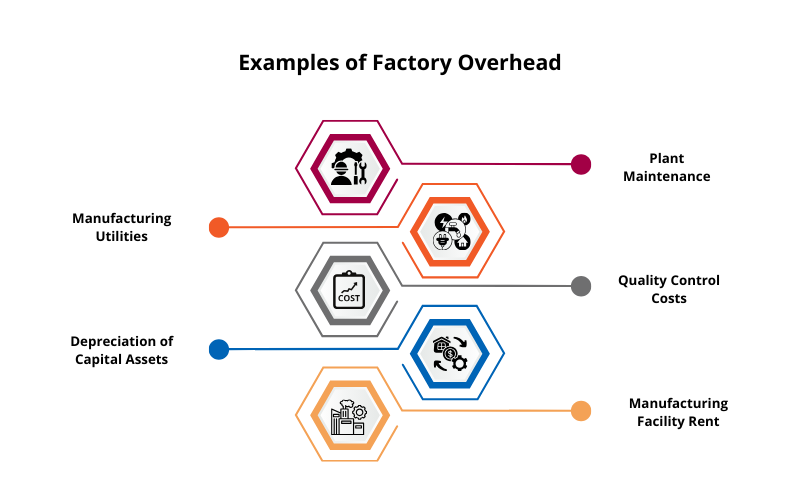

Common Examples of Factory Overhead

Now, let us discuss some of the popular examples of Factory Overhead:

1. Plant Maintenance

Plant Maintenance includes all those repair and maintenance charges incurred to maintain a facility. This includes wiring, electrical repairs, pool cleaning, repairs of Air Conditioners, lawn care, wages paid to contractors, and other related charges.

2. Manufacturing Utilities

Manufacturing Utilities include costs such as electricity, water, and gas, among others. Businesses incur these costs to run their day-to-day factory activities. It’s possible to reduce these costs by analyzing the spending patterns, negotiating with supplier companies, imposing usage restrictions, and initiating long-term deals.

3. Quality Control Costs

In today’s era, every business strives to manufacture high-quality, reliable, and safe products. They appoint quality control officers to oversee the manufacturing process and ensure their products meet the quality benchmarks and industry standards. Salaries paid to these officers, and other research and developmental costs associated with quality assurance, are classified under Quality Costs.

4. Depreciation of Capital Assets

Capital assets such as buildings, machinery, computers, and office equipment lose their value over time. At one period of time, their value becomes zero. Depreciation is an accounting method used to evaluate and assess the value of an asset. There are multiple types of depreciation such as Straight-line Depreciation, Units of Production Depreciation, Double Declining Depreciation, etc.

5. Manufacturing Facility Rent

Companies have to pay a fixed sum of the amount for using the factory space to the proprietors of the premises. This amount is predefined in the contractual lease agreement signed between the two parties. It is usually payable on a monthly, quarterly, or annual basis. Several factors can affect factory rent such as the proximity to transportation, the age of the building, etc.

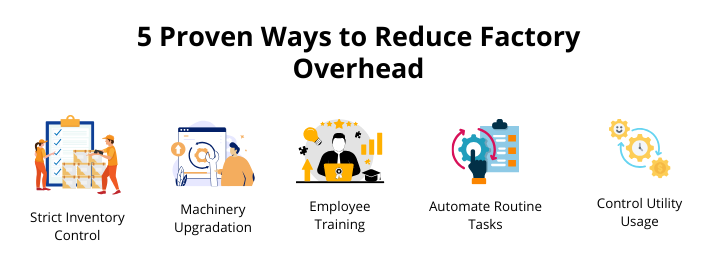

5 Proven Ways to Reduce Factory Overhead

Now that we’ve discussed everything from what is Factory Overhead, Factory Overhead formula, and its examples, let’s discuss various measures to control it.

1. Technological Modernization

The factory machines start to degrade over time. This degradation affects their performance, reliability, and safety. Upgrading older machines can help you achieve increased production scale, improve the factory’s capacity, and reduce Manufacturing Overhead.

2. Limit Utility Consumption

Conduct an energy audit and evaluate the power consumption pattern of your machinery. Replace traditional machinery with energy-efficient devices and upgrade the technology to reduce power consumption. Moreover, there is a need to increase employee awareness for adopting good practices (such as hibernating their PCs when they’re not in use for a long time).

3. Strict Inventory Control

Inventory is considered the lifeblood of any business. Adopting inventory management software will help you maintain optimum inventory levels. This will help you reduce inventory costs, improve cash flow, increase operational efficiency, and control Facility Overhead.

4. Workforce Training

With the introduction of new technology and tools, employee training has become more essential than ever. Money spent on employee training isn’t wasted; instead, it pays off with quality work, reduced human errors, and improved engagement.

5. Automate Repetitive Tasks

Another way to reduce Manufacturing Overhead is to automate routine operations through ERP implementation, Artificial Intelligence, and robotics. Leveraging modern technology will help you improve workflow, reduce Facility Overhead costs, and lower waste.

Which Expenditures Are Not Included in Factory Overhead?

After discussing Factory Overhead meaning, let’s discuss which expenditures are not considered a part of the Factory Overhead.

1. External Administrative Expenses

External Administrative Expenses include expenses incurred for administering a business that is not directly tied to the production activity. Common examples of External Administrative Expenses are costs paid to third parties such as office water & electricity bills, office rent, procurement costs of office equipment, and professional fees, among others.

2. Office Staff Expenses

The office staff expenses include a range of expenditures including gross salary paid to the employees, payroll contributions, overtime, employee insurance, provident fund, bonuses, and training. Furthermore, it also includes the cost of recruiting new employees.

3. Product Material Cost

Product Material Cost includes expenditure incurred for the materials used for the production. The actual cost may depend on various factors such as the quality of the materials, quantity, and type. Examples include protective wrapping, boxes, and labels.

4. Direct Labor

Direct laborers are involved in the actual production activity in contrast to the regular office employees who may be involved in office administration, maintenance, and customer support activities. Wages paid to direct labor are not included in the Manufacturing Overhead.

5. Marketing Costs

The marketing and promotional expenditures include the costs incurred for promoting the company’s goods and services, money spent on advertisement (such as newspaper, TV, and Internet), sponsorship, merchandise, display ads, branding, and salaries paid to the marketing & sales departments.

Summing Up

Factory Overhead is an important metric for managing your business’s manufacturing operations and identifying any indirect costs associated with your products and services. ERP Software can help you in different ways from controlling costs and setting better & realistic pricing strategies to gaining competitive advantage.

Sage X3 is a multi-company, multi-country, and multi-currency solution that comes with a robust set of features. It brings efficiency to your business activities, helps you respond faster to changes, and supports seamless global expansion. It brings efficiency to different business operations such as supply chain, procurement, inventory control, customer support, financial management, and so on.

FAQs

1. What is Factory Overhead Meaning?

Factory Overhead is the sum of all indirect expenditures incurred for the smooth production of goods. It is an operational cost that includes a combination of fixed, variable, and semi-variable overheads.

2. Are Factory Overhead & Direct Cost the Same Concepts?

Factory Overhead and Direct Cost are not the same concepts. Direct Cost is the cost of producing a specific product such as direct labor, direct raw materials, etc.. In contrast, Production Overhead is not assigned to any specific product. It may include rent, depreciation, and utility bills.

3. Can Factory Overhead Affect My Company’s Financial Statements?

Production Overhead can affect your company’s financial statements. For example, lower Factory Overhead can reduce the Cost of Goods Sold (COGS), thereby increasing profits in the Profit & Loss Statement. Moreover, it can impact equity, current assets, and working capital requirements in various ways.

4. How Does Factory Overhead Affect Product Pricing?

Calculating Facility Overhead gives decision-makers an edge over their competitors. They can offer better competitive pricing, reduce manufacturing costs, and prevent underpricing or over-pricing of their products for optimum delivery rates.

5. Which Costs are Incurred for Manufacturing a Product?

The costs of manufacturing a product may differ from product to product. It may include wages to factory laborers, cost of the raw materials procured, research & development cost, production factory rent, and so on. While some of these costs are direct, others are indirect in nature.